The global market for rail vehicle maintenance continues to grow. It is increasingly recognised by rolling stock manufacturers as an attractive business that helps reduce volatility and promises predictable long-term revenues. Whereas in the past the maintenance and repair of rolling stock was almost exclusively the responsibility of the railway operators, there is a growing willingness on the part of the operators to enter into long-term maintenance contracts with the industry and to concentrate on their core business of transporting passengers and goods. This is shown in the latest study "Rail Vehicle Maintenance - Global Market Trends in the After-Sales Market 2023" by SCI Verkehr.

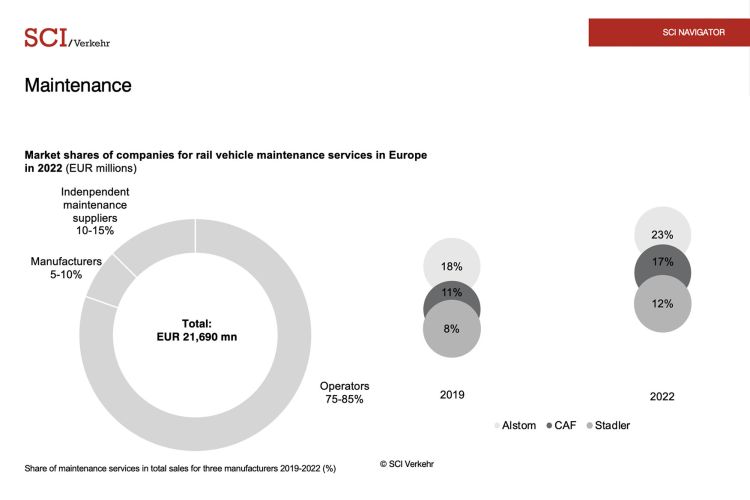

The established state railways operate the largest fleets in both passenger and freight transport and rely on their own maintenance network. Depending on the segment, they will account for between 65% and 95% of the European market volume in this segment in 2022.

However, competition in the railways' core business is increasing. As a result, operators are reviewing their cost positions and, due to demographic changes and a shortage of skilled labour, are more willing to leave maintenance and the necessary investment in workshops and personnel to the manufacturers. In addition, maintenance requirements are changing significantly as drive systems change. Diesel vehicles are being replaced by battery and hydrogen powered vehicles with new maintenance requirements. In order to meet the changing market demands, established operators need to upgrade both their staff and equipment, study concludes.